South Africa specializes in insurance, partly due to our culture of high crime & fear of public hospitals & death and partly due to our smartest people taking on the challenge of studying actuarial science. Over the last 4-5 years or so there has been an increase in insurance-focused Startups, innovation last seen in ‘92 when Adrian Gore left Liberty to start Discovery.

The interesting thing here is the relationship between incumbent organizations and their disruptive counter-part. You see, dating back to ‘92 when the Cofounder of Rand Merchant Bank(RMB), Laurie Dippenaar gave Adrian Gore a 10 million rand cheque for his idea and incubation space at Momentum, Corporates backing insurance startups has been the catalyst for innovation in this space. RMB would do it again in ‘96 when they funded Outsurance and the rest is history.

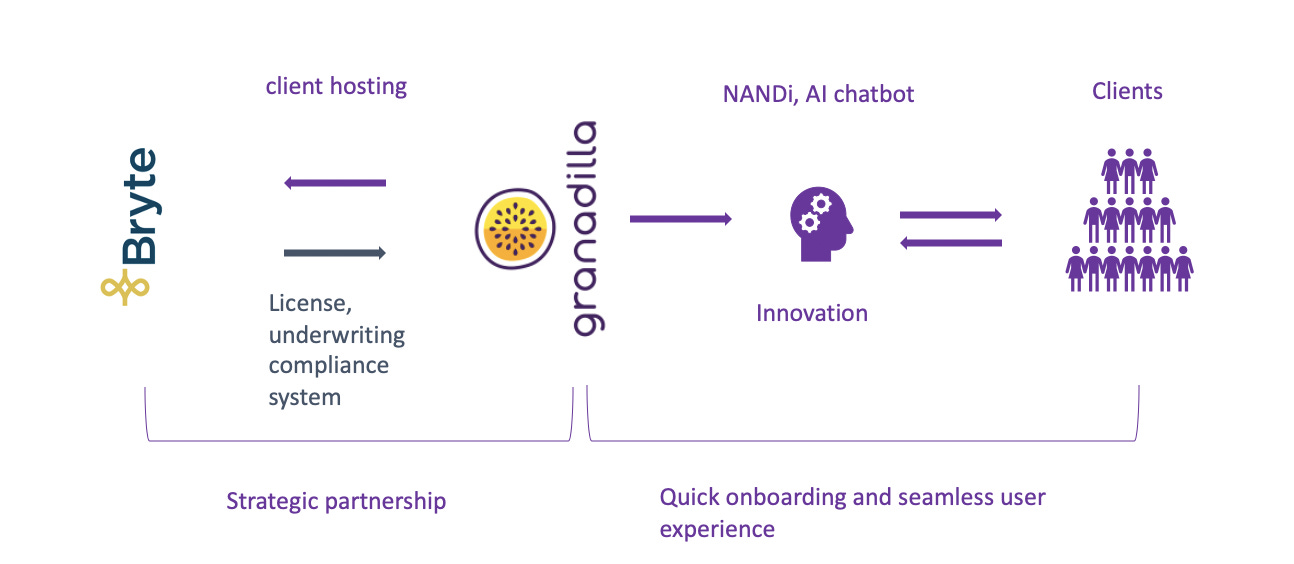

Back to our title! Let me start with the lesser-known one, which I must admit is my cellphone insurer of choice; Grandilla.ai. Founded by a guy called Jonathan Walker after a bad claims experience when his phone & laptop were stolen. Granadilla uses AI chatbots for client interactions so it doesn’t need to invest in a massive call centre infrastructure; this goes for all these new players. Its onboarding chatbot is called NANDI she’s quite helpful in a somewhat seamless onboarding experience where you just take a few snaps of your phone (you probably need another one to do that), accept the terms & conditions and you’re covered in less than 24 hours. The reason that Granadilla can do this is because of technology and the advancement of AI & AI chatbots, with a little help from Bryte insurance.

The relationship with Byte is strategic in nature, Granadilla gets to piggyback off their license and compliance system + an investment, and Bryte gets possibly a fee from each contract. This symbiotic relationship has allowed Granadilla to innovate and grow its base – the last time they released numbers was July 2019 when that had 30 000 downloads a year after they launched, I’m sure this number has continued to grow since then and hopefully, they were able to convert those downloads into paying clients.

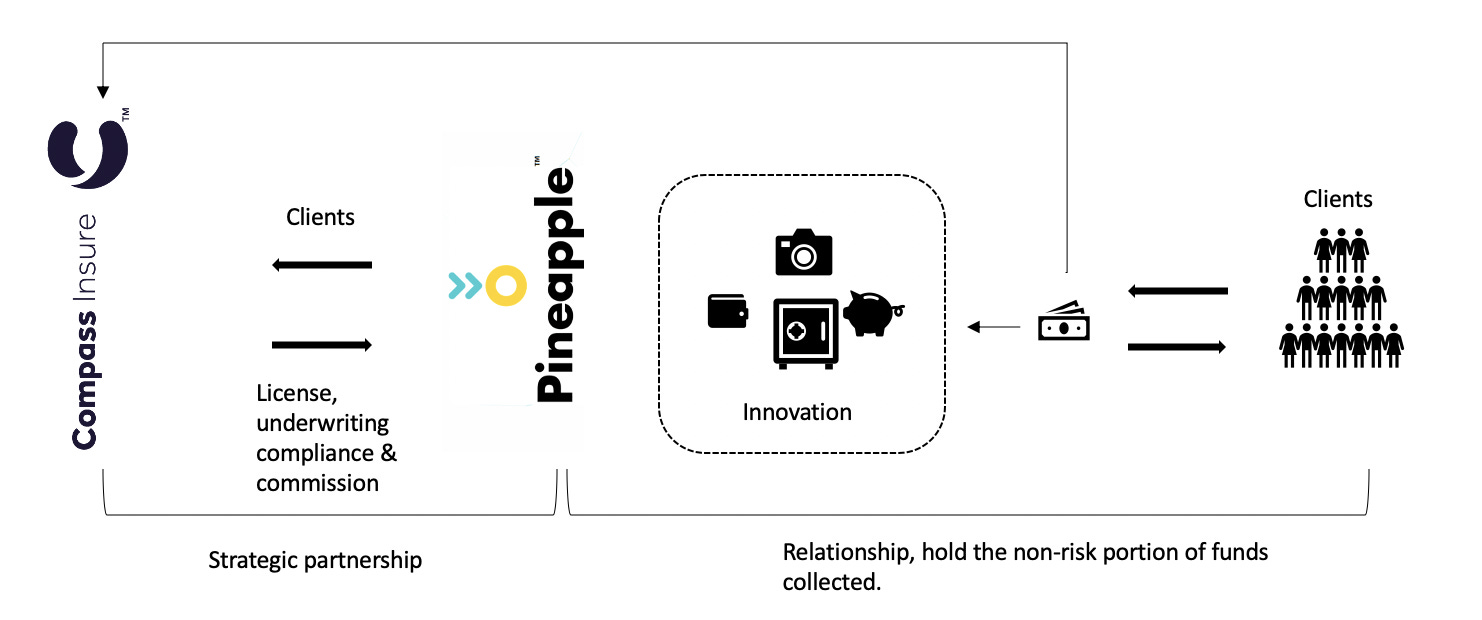

The other fruit insurer is the well known Pineapple Insurance🍍, founded by 3 young gentlemen, Matthew Smith, Ndabenhle Ngulube and Marnus van Heerden, quick one, there’s another ‘fruit’ insurer in the US called Lemonade, funny right!. I digress, this was after they entered into a competition hosted by Hannover Re, a reinsurance company and the startup’s first backer; they have since gone on to win an innovation challenge that led to a $1.5 million prize money.

Pineapple works like a wallet, where the money you pay in premiums for your devices goes into a digital wallet and if something happens to assets you can claim from that wallet, you can also choose to share risks within your network vis-a-versa, Its called peer-to-peer insurance or social insurance if you want to rephrase it, pretty neat.

This type of innovation is at the heart of millennial culture and the belief that capitalism is inherently social. I do not doubt that pineapple will become a large organization one day, especially with the move to the USA.

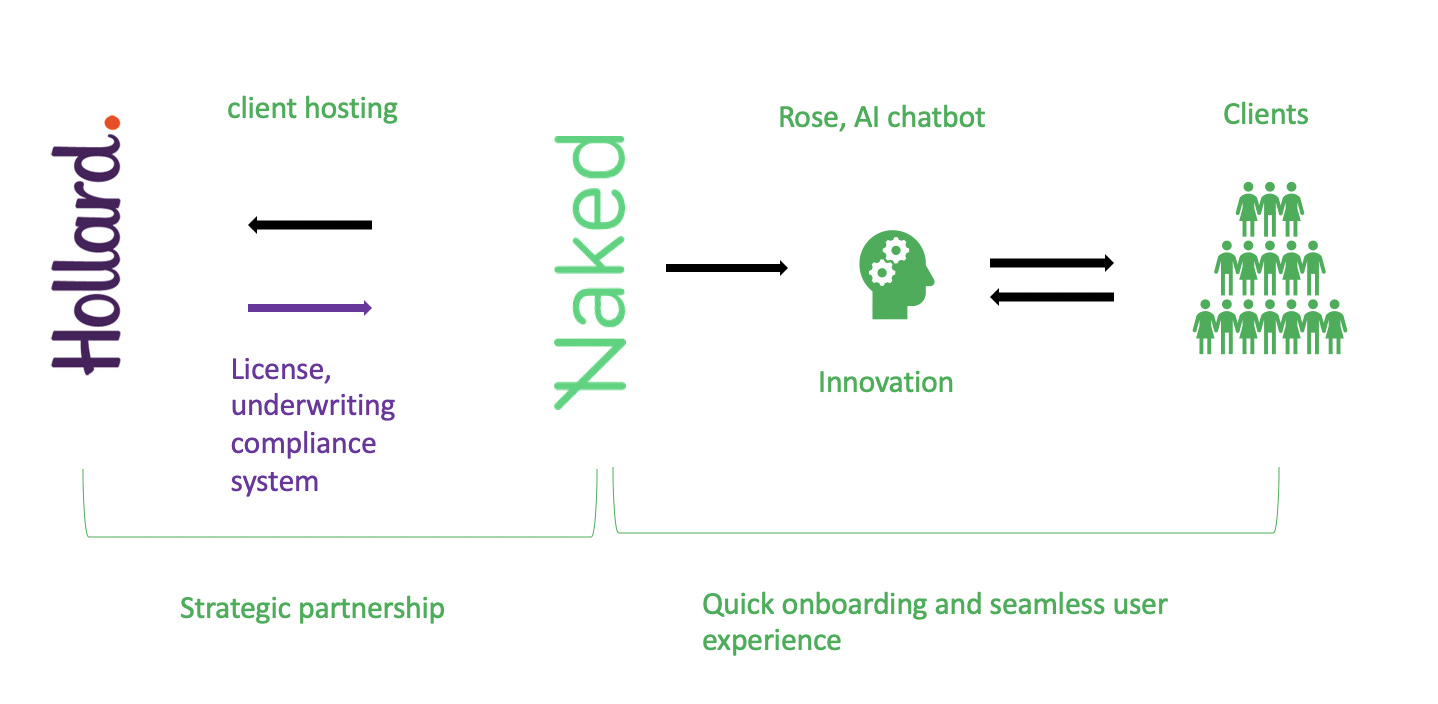

Naked Insurance is a bit different from the two fruit insurers but still has a similar model to Granadilla. They decided to take the route of car & household content insurance first, a hyper-competitive market where money speaks louder than catch phrases. The beauty of car insurance is that consumers are not loyal to brands only price tags but Naked seems to be hitting it out of the park. It’s another beneficiary of Corporate backing, funded by one of South Africa’s richest and reclusive families, the Enthovens, founders of Hollard Insurance & owners of Nandos🍗 with the backing even extending to headquarters. Naked is in the same building as Hollard.

Naked was founded by 3 seasoned actuaries, Sumarie Greybe, Alex Thomson, & Ernest North after the former pair left their jobs as partners at the accounting firm EY. Since the company was founded in 2016 and officially launched in 2018, it has grown exponentially, I estimate that they should have reached 200 000 monthly active clients by now, up from 83 000 the previous year and 15 000 the year before.

Essentially, the problems these insurers are trying to solve are the same: Poor customer experience at the hands of incumbent insurers with the hope of making the purchase of insurance less … grudgey.

Innovation will continue in this space with the help of existing players forming symbiotic relationships with Startups as long as South Africa produces those crazy Actuaries.

Thanks for reading, feel free to comment,

Take care.

By Ububele Kopo