Agriculture, like education, hasn’t changed much over the last 100 years or so (when I say agriculture, I am referring to farming, forestry, fisheries & agri-processing). Today, the agricultural market in SA amounts to about $11bn, approximately 3% of total GDP. Listed companies make up approximately 4% of the JSE’s $670bn market cap ($26.8bn) this includes some Fast Moving Consumer Goods (FMCG) companies & most (farming, fisheries & agri-processing) companies are small to medium cap < R10bn — Its a big niche market (oxymoron intended).

For us to move forward we need to look at the past

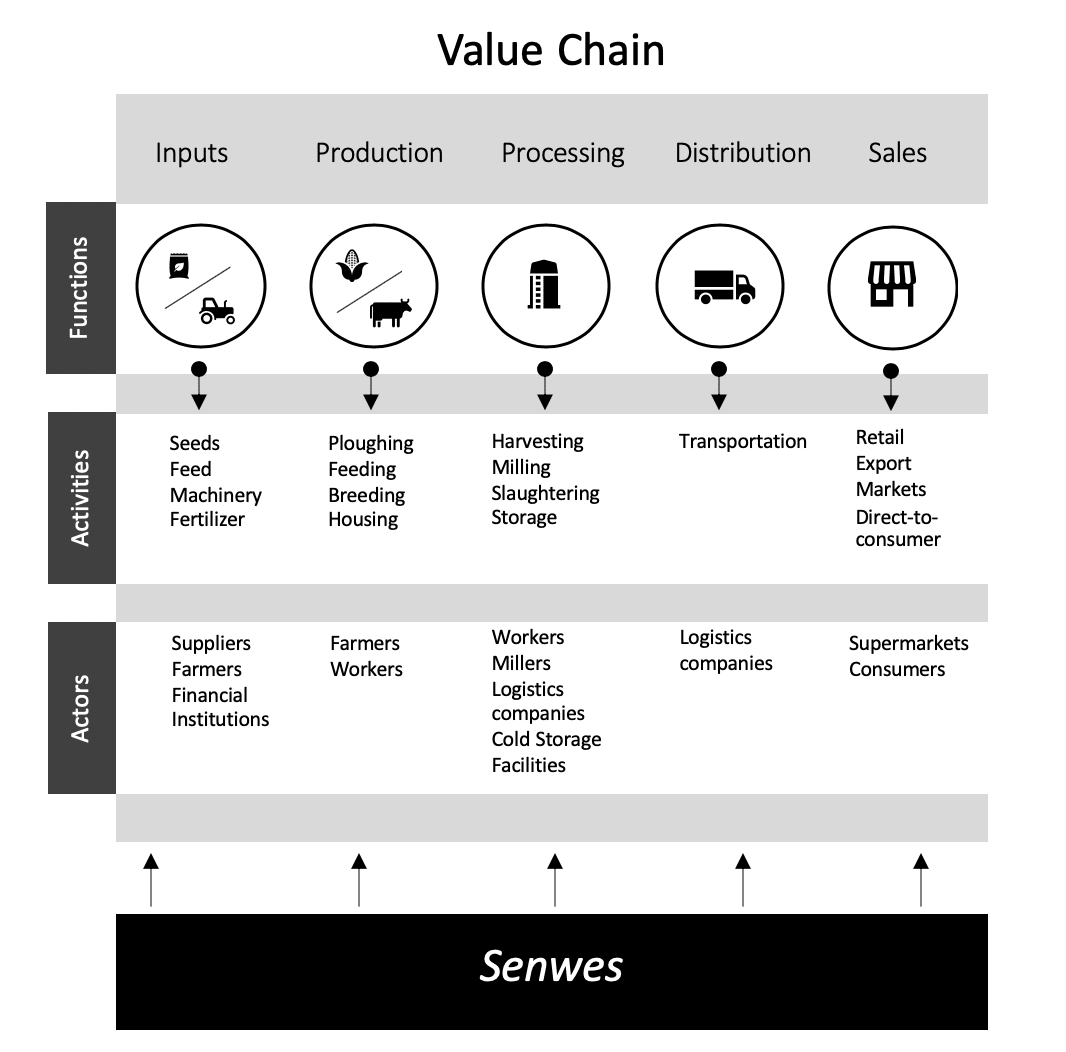

INTEGRATING THE VALUE CHAIN:

Inputs, finance & markets — these are the bedrock pillars for agriculture & for over 100 years agri-services firms have been integrating the value chain.

What does the agricultural value chain consist of? For the sake of oversimplification, the value chain consists of 5 core functions:

Inputs > Production > Processing > Distibution > Sales

In each function, there are activities that require certain actors. For instance, in distribution the activity is transportation & the actor would be a logistic company.

There are a lot of businesses along the agricultural value chain, so where does one start in the value chain? At the beginning, of course; Inputs — the land, the seeds, the infrastructure — without a farm there’s no production, there’s no processing, there’s no distribution, & there are no sales.

Inputs require capital, they go hand in hand, therefore in 1912, an institution was created for such. Its mantra was, “to serve South African commercial & emerging agriculture by bringing specially designed financial services within the reach of farmers across the nation”, & so the Land Bank of South Africa (LADBSA) was born.

By fortifying the marriage between inputs & capital, agri-businesses were allowed to kick start the interlocking. Hence, value chain integration was the underlying idea that led to the formation of each organisation mentioned at the beginning. Senwes was started as a co-operative in 1909 & the first seven directors were elected. I’ve never thought of farming as a normal business that has an organisational chart, departments, cross-functional work & board of directors. I always thought about it as a one-person endeavour or a co-operative with members doing the same thing.

“From the beginning, each of the directors was charged with various duties. For example, Omne regularly had to liaise with the Central Agency in Johannesburg as the marketing arm of cooperative associations, while another director had to report with regard to the functioning of stores” – Time Cultivates Winners: Senwes a century of agriculture by Elize van Eeden.

In 1924 South Africa created its first grain silo, the now Silo hotel in Cape Town, famous for the port grain elevator. Prior to Fred Hatch creating the first vertical grain silo in 1873, grain was stored in barns. Young Fred had discovered silage from sugar beet, maize & pulp & wanted a place to store it (silage is basically pickled grass). What young Fred learned was that if he created a silo structure above ground this would keep the silage & maize, dry & cold thus healthier for cows which would lead to increased output of milk. Young Fred & his father built 3 wooden silos in 1876 & in 1893 the first steel silo was exhibited in Chicago, Illinois.

Why is this important? because agri-processing contributes significantly to the top line of agri-groups. In 2019 Senwes generated R4.95 billion in revenue before intergroup sales of that R3 billion came from grain-linked activities. Within agriculture, there are different types of processing for different activities but I want to focus on maize, please bear with me.

Since 1924, South Africa has created 432-grain silos. From the 1950s till early 1990s grain storage & marketing was controlled by marketing boards who were controlled by the government under the Marketing Act of 1968. Then control was passed back to private companies & co-operatives like Senwes converted to private companies when the change took effect under the Marketing of Agricultural Products (MAP) Act (No. 47) in 1996. Today there’s grain capacity of 16.3 million tonnes, of which 85% is owned by private companies. Of the 432 grain silos, 172 are on farms, but they are small, some hold less than 100 tons, 260 are commercial. These 260 commercial silos have 17 owners, together account for 93% of all grain capacity, with 3 owning 73% of the total grain capacity, which 3? NWK, Afgri & of course Senwes.

Agri-processing, in maize, is big business but only for a few; the value chain is integrated.

In the 1950s when the marketing boards controlled the maize industry, they used to control freight to & from the farmers for maize. If the distance was more than 80km the marketing boards were mandated to use rail; rail was & still is owned by the government. When control passed to the co-operatives, they invested in logistics & export.

To understand where we are going we need to understand where we come from, this might not be what I normally write about but it’s important to give context for what I plan to write about. The future of agri-business is in unbundling the farm. Stay tuned for part 2 next week.

Take care.

Bu Ububele Kopo