This piece was inspired by a blog post from Root Insurance’s founder Louw Hopley titled “What it takes to start selling insurance”. I’ve personally had a love-hate relationship with insurance, on one side it is an essential aspect of wealth creation & protection for the middle class. On the other side, insurance as an industry has a conflict of interest due to the zero-sum nature of the relationship between policyholders & insurers, plus the misalignment of incentives between policyholders & brokers. It is one of the only industries that’s mandated to have a conflict of interest policy. Nevertheless, insurance is an essential element of any society that wishes to grow, people simply must protect their assets.

I spent some time in December looking at “How to build an InsurTech” after a few people asked me how & realising that most, if not all, InsurTechs in South Africa were practically insurance brokers as opposed to fully licensed insurance companies. I also discovered that there is a playbook for how to go about building an InsurTech.

I think this is where I put a disclaimer that; no I have not built one & this is merely based on my research, there is no substitute for execution, it takes a hell of a lot to build a company. We have some exceptional InsurTechs in South Africa; Pineapple, Simply Financial & Naked being at the top of the field.

💡 Thesis

To start off you need a thesis about what’s wrong with insurance. As stated, insurance companies have an inherent conflict of interest, this causes tension in the relationship with their policyholders & heightened when people need to claim. Most people view insurance as a grudge purchase, a necessary evil. This is where the gap arises for new players in the market who seek to rectify & change the nature of the relationship through business model innovation or incorporating some behavioural aspect to change how risk is priced. There are two popular theses’ (that also didn’t sound right in my head) that most InsurTechs use:

- Insurance is broken because of the conflict of interest between policyholders & insurers, we plan to rectify this by removing the conflict & taking a fixed fee on the premium, pooling funds for claims & either donating the surplus or returning the unused premiums to clients.

- People pay too much for insurance even when they don’t need to. So instead of charging people premiums when they don’t use their assets, let’s make cover on-demand so they only pay when they actually need to.

The first one was popularised by Lemonade insurance in the US & the second one has been around a bit longer, popular with car insurance, it’s called pay-per-mile.

Once you have your thesis in place you can test it with your intended customer base. This can be done via customer development; for this, I’ll refer you to Steve Blank’s Four Steps to Epiphany. As you do this you need to build a business case for how this is going to work; oh & money, you need money.

📄 FSP License

At this stage you need an FSP, you’ll quickly realise the regulatory hurdle of being a fully licensed insurer carrier. But you need to start somewhere so a FAIS accreditation is where you start. Here is when you need to do things concurrently by seeking an Insurer & their Reinsurance partner to help you to start building the product you are going to sell customers.

For an FSP license, you need to get through some paperwork with the Financial Services & Conduct Authority (FSCA). For help, you can contact Masthead, Moonstone, The Compliance Toolbox or Compliserve. There are five category types for the FSP license (category I, II, IIA, III, & IV). Category I, intermediary short term personal lines is the main one for InsurTechs. You can establish if you meet the criteria to be a Key Individual (KI) for the FSP license, if you don’t meet the criteria you can either do the course work & exams & required experience or get a co-founder who can be the Key Individual (KI).

Here’s the list of things you need to cover:

Category I application process via Masthead.

- Registration documents for the legal entity (CC or Company from CIPC) or Trust Deed and Letter of Authority.

- (Trust)

- Certified copy of Identity Document (of each KI)

- Certified copy of Highest Qualification (recognised Qualification) of each KI

- Certified copy of RE certificate(s) (RE1/RE5) of each KI

- Short CV of each KI

- Reference letter(s) for KIs reflecting management experience and experience in categories and sub-categories being applied for

- Role of KI in the business

- Business Plan (i.e. how business will be conducted) / Business Strategy

- In the case of a new entity, projected financial statements for a 12 month period is required and confirmation from auditor or accountant, whichever is applicable, that the entity has not traded.

- If Long Term Insurance: sub-category A (sub-category 1.1) is selected, provide the names(s) of Assistance Business FSPs and/or Long Tern Insurance companies with whom the business has agreements.

- If applying for Health Service Benefits, the Accreditation Certificate for both the entity (if applicable) and each Key Individual to be appointed for this product category, is required.

- Proof of payment of the application fee (R2500~$167)

Approval will take some amount of time this is why its important to do it as a team.

🏢 Insurer & Reinsurer

You cannot have an InsurTech without an insurance partner. Insurance companies in South Africa have a friendly relationship with InsurTechs and are generally open to working with them:

*Pineapple has switched over to Old Mutual to build a car insurance product & a new InsurTech called OneSpark works with Guardrisk.

Insurance companies help with underwriting & have the balance sheet & staff of Actuaries to validate your thesis. According to Louw, you have three options:

- “Get your own insurance license. This is typically too costly and compliance heavy for most businesses, even at the scale of a national enterprise. It only makes sense if insurance is your core business, not if it’s a supplementary business.

- Resell an insurer’s existing products, meaning you act as a broker and resell products that exist in the market. This approach is not ideal for a few reasons: no customisation or white-labeling, limited or no APIs, revenues are limited to commissions, etc.

- Partner with an insurer that specialises in 3rd-party partnerships, like a cell-captive insurer. This is the approach we suggest.” – Louw Hopley, Co-founder & CEO of Root

I am not sure of the economics of the relationship with a cell-captive insurer but you share the risk & potential losses so if you don’t have that much money option 2, with a twist is the right one for you. You can work with one insurance partner & act as the broker for the product you co-create. Let’s say you go with Compass Insurance & co-create an insurance product based on your thesis, you will now act as the broker for that product & take a commission for each product sold. This works well with your thesis & Compass Insurance because they get a new client base & some underwriting profit.

📊 Business Model

The business will differ based on the chosen insurance sector you want to operate in. Because you’re a Category I no advice broker that business model is limited to commissions earned. Short-term insurance is a R100 billion (~$6.7 billion) in Gross Written Premiums market. Healthcare is a R220 Billion (~$14.7 billion) in Gross Contributions market & Life Insurance is a R140 billion (~$9.3 billion) in Gross Written Premiums market. The commissions are set by law, so if you are an InsurTech in short-term, healthcare or life, the economics will be different:

- Short-term = 12.5% on motor & up 20% recurring commission others (contents, household etc)

- Healthcare = 3% of contributions up to R69 plus VAT, recurring.

- Life: there’s a calculation for it based on years to retirement but under the age of 38 it’s roughly 10 times the monthly premium for the first year. *depending on the insurer it could be more. *differs for non-mandated intermediaries.

How does the commission work?

- Short term: Average short-term insurance premium (car) is R900 so R900 x 12.5% = R112.5 per month.

- Healthcare: Average open scheme healthcare contribution is R1600 so R1600 x 3.5% = R56 per month.

- Life: Average Life cover costs approximately R20 per day (R600pm) x 10 = R6000 upfront for the first year. *depending on the insurer it could be more. *differs for non-mandated intermediaries.

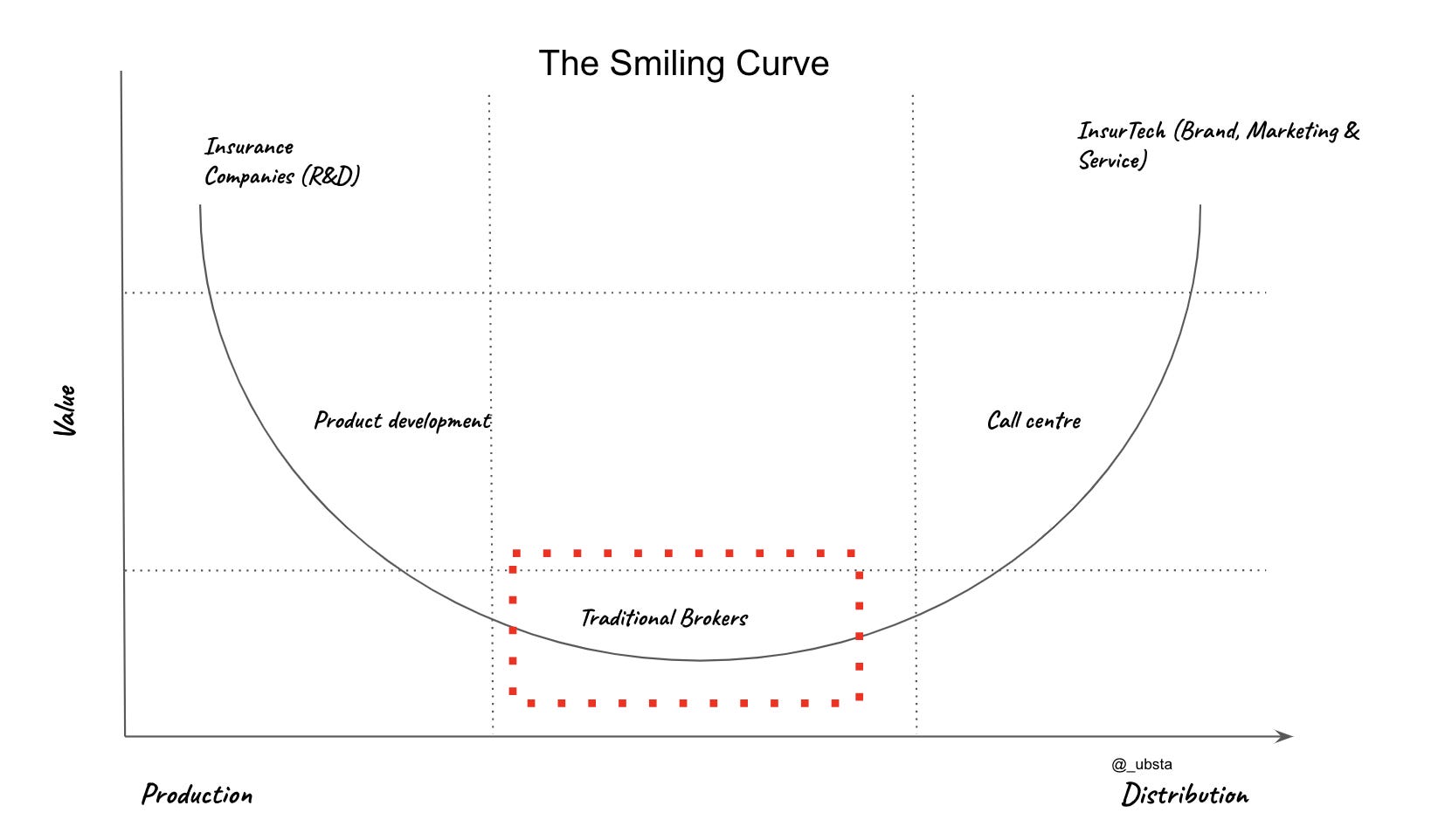

⚙️ Policy Administration & Claims Management

In the process of building out the product (technology), you will need a sort of engine/operating system, a platform to administer policies & manage claims. Certain insurers have their own, some outsource it to a third party like Brolink. The future for InsurTechs (& Enterprises) looks more like building on top of Root’s platform. Root is an API driven Insurance as a Service platform (I know this might sound like an ad for Root but it’s not, I’m just a fan of what Louw & his team are building).

This will take most of the burden off you & your tech team to focus on the core user experience & distribution without worrying about the system breaking down in the early days, there’s enough value in the distribution, brand & service to make the endeavour a venture scale.

This is how I see the market going:

📱Technology

The use of chatbots has been uniform in the industry. Lemonade Insurance introduced the 2 chatbot method – 1. for onboarding & 1. for claiming. This works for short-term personal lines, Antoine at Finchatbot can help you out with this. Another way for car insurance is the smartphone can be used as a telematics device. For life insurance, the innovation can be a fast and seamless onboarding experience & instant payout in case of death, disability or severe illness.

But focus on your core thesis & the customer to help guide the product experience. Use AI & Machine learning to continuously optimise the experience for customers (easier said than done).

👭Customers

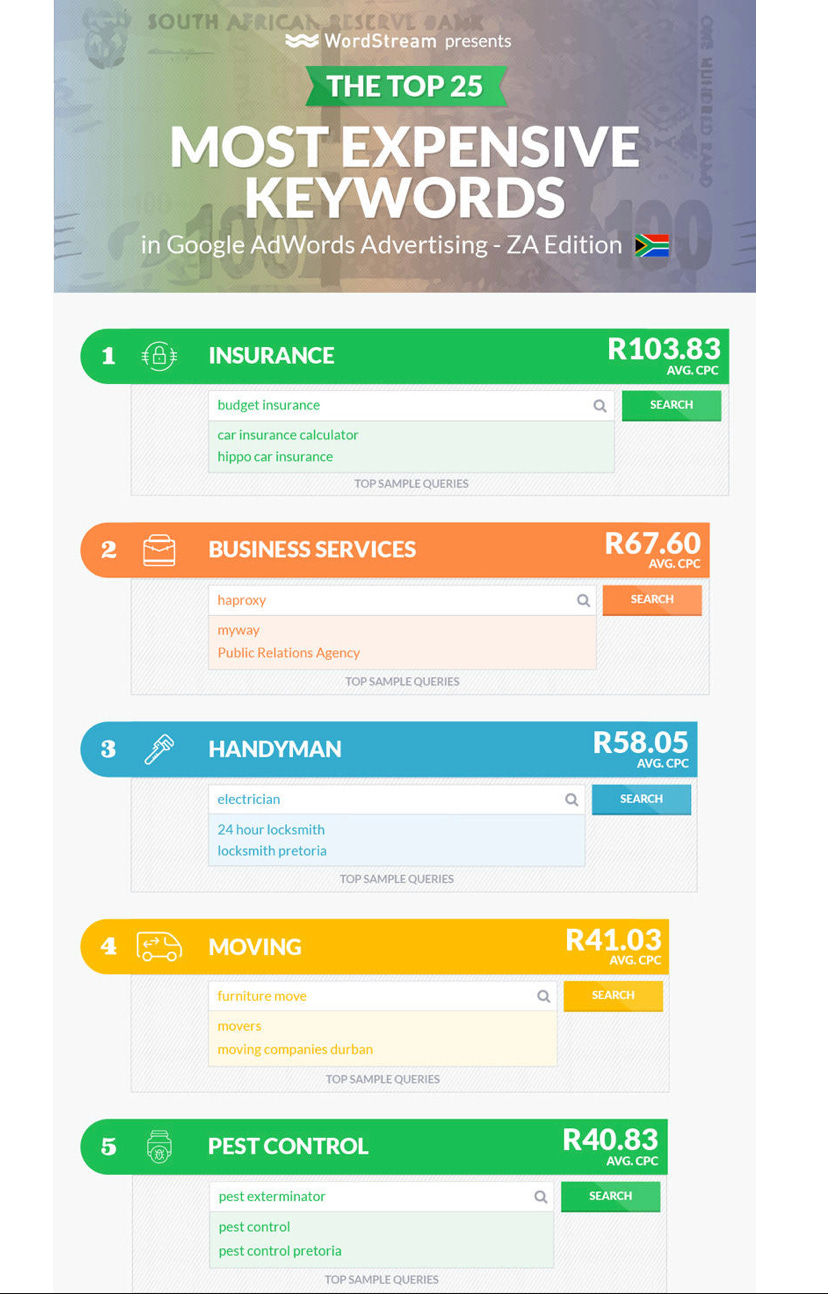

The most important reason for building an InsurTech is to provide the end customer & their family a better experience from what exists in the market. This means making sure you build for them & treat them like the people they are and not like a policy number. In fact, you should start off before you even do anything by understanding who the core customers are. It’s important to establish a proprietary distribution channel, Google & Facebook will not be your friends. ‘Insurance’ is notorious for being the most expensive Google adword in South Africa, the cost per click (CPC) is over R100 (~$15) so your competitive advantage should be compelling enough to drive organic growth. Content & partnerships should be your friend. This goes back to the alignment of the product with your core customers.

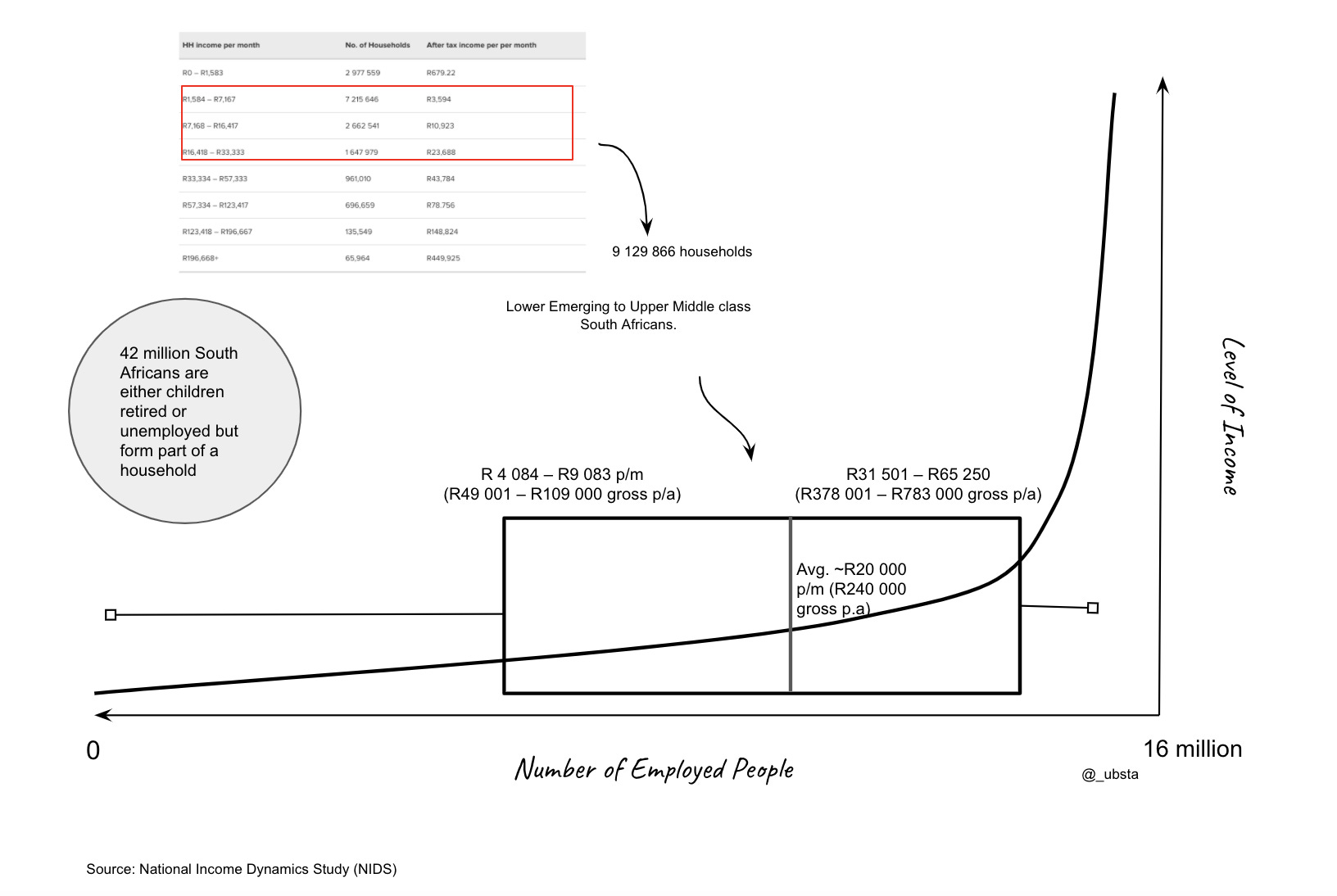

My personal belief is that insurance is most important to the emerging to upper-middle-class because those households are often one mistake away from financial distress in the quest for financial freedom. The emerging to upper-middle-class income households are often one death away from a drastic lifestyle change. Protecting everything around their main source of income is thee most important thing to ensure the next generation does not live a life of poverty; that means fewer funeral plans & more life plans. That means more car & household insurance cover & that means more affordable healthcare.

By Ububele Kopo

Take care.