Each Monday Morning Ububele shares a newsletter about tech-enabled startups in South Africa, or how certain technology trends might be relevant for South Africa & sometimes the founding story of innovative companies. This week he wants to stretch your brain for a bit. He’s been obsessing about building an organization that can last 100 years for a while now. And he thinks he’s have found a way that can happen. The next 100-year company will be a crypto-based insurance company. Let’s find out how & why it will & should be built in South Africa.

Mutual Assurance Societies

Insurance companies, like banks, don’t change — at least in function. This is because Insurance companies are in the business of buying risk & risk has been around for a very long time. Insurance companies have not always been profit-motivated machines, before the 1980s most insurance companies were Mutual Assurance Societies. Mutual Assurance Societies are one of the oldest organisation forms in the world. In South Africa, some of the oldest companies are Mutual Assurance Societies. RandMutual is 140 years old, they still do workmen’s compensation for miners. Assupol Insurance, which demutualised in 2010 has been around for 108 years, they provide funeral, life, savings & retirement products. FemMutual is 100 years old, they still do workmen’s competition for healthcare workers. Another one, AVBOB, a 102-year-old Mutual Assurance company focused solely on Funeral benefits still exists in its original form, governed by the AVBOB Mutual Assurance (private) act of 1961.

What is a Mutual Assurance Company?

“A mutual assurance/insurance company is an insurance company owned entirely by its policyholders. Any profits earned by a mutual insurance company are either retained within the company or rebated to policyholders in the form of dividend distributions or reduced future premiums. In contrast, a stock insurance company is owned by investors who have purchased company stock; any profits generated by a stock insurance company are distributed to the investors without necessarily benefiting the policyholders.” – wikipedia

The Mutual Assurance/Insurance company concept comes from 17th century England & has been exported as part of the British Empire to most Commonwealth countries. This is why insurance in South Africa is very similar to insurance in other commonwealth countries that have embraced insurance like Australia, Canada, India etc

Mutual Assurance companies were born from a broader concept of Mutual Societies, which have the same properties at the core, which is being owned by its members. They differ in how business is conducted, some examples:

- Building Societies – mutual society for mortgages

- Credit Unions – Cooperatives that provide banking products like deposit accounts & credit

- Friendly Societies – mutual society by communities (ROSCA or Stokvel)

- Mutual Savings Banks – Bank owned by its depositors.

Now imagine if this type of organisation existed & was governed by nothing more than code & self-executing smart contracts. Would an AVBOB for the internet survive 100 years? I think so, but for that to happen, success needs to be articulated and implemented in a manner that is native to what a successful crypto-based project looks like.

Components of crypto success

According to an American Investor, Jesse Walden, crypto-based projects have 3 components of success with the ultimate goal being progressive decentralization.

3 components of crypto success:

- “Product/market fit

- Community participation

- Sufficient decentralization (community ownership)”.

Product/market fit

Like all startups, it has to start with building something people want. Now, it’s still unclear how millennials feel about insurance, in particular, funeral cover in South Africa. It’s an old product that is institutionalized within the black population across all cultures in South Africa. funeral plans have been stable for the black household for over 100 years. Funeral Insurance is not going anyway but how it’s delivered will change.

Community Participation

Crypto projects are heavily reliant on community participation for the success of a project. The idea of community participation results in derisking the platform from decisions that hurt users. This stems from what happens with Web2 platforms like Facebook & Twitter. Enhanced participation in governance which results in the alignment of incentives & network effects. This is present in the cooperative economic model & the mutual society model because the users are also the owners.

Sufficient decentralization

The last step of a crypto project’s success, after product/market & community participation, is sufficient decentralization of the project. To be honest I’m not quite sure this matters for most projects given the complexity of some, maybe for on-chain projects & protocols but exciting to the community is the last step in progressive decentralization. This can happen fast via a fair launch or even take a decade but the ultimate goal is token distribution. Exiting to the community can be contrasted to an acquisition or even an IPO in the crypto sense.

Crypto projects are an experiment in governance with risk, value and incentives. This has benefits for first principles thinking. A way to re-imagine the existing legacy financial system. These benefits are highly correlated to insurance.

Benefits of a Crypto-Based Project

A crypto project has a few benefits compared to the traditional legacy financial system. This is not to say it’s better than what exists in any way, it is still early days and still unclear that crypto or better yet DeFi will ever get mass-market adoption but the benefits are noteworthy especially when you contrast them to the insurance industry. To touch on a few of them;

#1 Transparency— the use of public blockchains & open source technology allows for transparency, but not only the transparency of the transaction layer but the transparency in operations through governance. Customers can now see what the organisation does with their premiums & have an input on how it is governed.

#2 Trust-less Consensus — As weird as that sounds, the most important aspect of public blockchain technology is the trust-less consensus it provides to the network & the communities built on top of it. This trust-less consensus is cemented by the most powerful of incentives; money.

#3 No Intermediaries — Insurance has long suffered from a conflict of interest problem, where if the customer claims the insurance company loses profit. The “solution” to this problem, funny enough, was to outsource distributions using insurance agents as intermediates to mend the information asymmetry gap the insurance company has vs the customer. Crypto projects completely break this down because of #1 & #2.

There are a few more benefits but I’m not sure if they are applicable for the purpose of our discussion.

Okay, so at the high level we have those 3 core benefits of crypto-project but those on their own are not a conclusive enough reason for a crypto-based insurance company. Let’s contrast them to the problems faced by traditional insurance companies.

Problems with traditional insurance

#1 — Lack of trust, it is quite clear that customers dislike their insurance providers and insurance providers see customers as a necessary evil to conduct business. This lack of trust causes administrative friction, where customers claim for everything so they can get as much value as possible for their premiums & insurance providers overburden customers with paperwork & exclusions in an act to curb fraudulent claims.

#2 — Competition; Insurance as an industry is overcrowded with providers with commodity products fighting for customers. This has caused many providers to compete on price and overzealous marketing gimmicks. This further erodes the relationship between customers & providers leading to no rapport, the relationship is strictly transactional.

#3 — Channel conflict; Insurance providers are at a crossroad between fully embracing digital channels for distribution vs investing & growing their insurance agent network. Currently, most are doing both but in about 10 years it will be clear that mobile is the more sustainable channel once they figure out how to improve the customer service & experience. This problem is why InsurTech innovation has increased over the last 6 years. InsurTechs, at least in South Africa compete directly with insurance agents but in time will compete with Insurance companies.

Again, these are generalised problems faced by most insurance providers. There are some issues that other people dubbed as problems incumbent insurers have like technology & tapping into younger millennials. I don’t agree with those because large insurance companies have adapted & adopted new technologies & as younger millennials & GenZ get older & start acquiring assets & babies, insurance will become an important part of their lives & thus grow into it.

But, what type of insurance companies will they gravitate to? it becomes less about value for money & more about a good experience plus value for money. New InsurTechs have sprung up to serve this market by using the primitive of shared-value but not embracing the primitives of new technology like public Blockchains. Pineapple Insurance was close to this, initially, the idea was an Insurance company on the Ethereum blockchain called Amie, but after conducting interviews during their design thinking process the team pivoted & applied for an FSP license & became a traditional InsurTech. Pineapple had the right idea, maybe the timing was wrong.

We can investigate & make a case for a new type of crypto insurance company with the focus being a Mutual Society that lives as an application on the Blockchain, a sort of Decentralized Autonomous Organization (DAO). An AVBOB for the internet.

AVBOB for the Internet

AVBOB is the biggest Mutual Assurance company in Sub-Saharan Africa with 2.2 million policyholders, 7 million lives assured, R21.4 billion in assets (~$1.4bn), R4.7 billion (~$313m) in premium income & R1.2 billion (~80m) in net income . . . a burial society. . . In 2021.

So why an AVBOB for the internet? At the base level, it’s 3 things, 1. Trust, between the organisation and the customer, 2. Efficiency, by automating the contracting & financial administration of an organisation more time can be spent on improving the experience and 3. Incentives, & incentives that are more modern to the internet native generation. According to Discovery, millennials in South Africa face an R15 trillion ($1Trillion) insurance gap, they call us MAROUNs, Millennials At Risk Of Underinsurance. Regardless, that gap can never be plugged with the existing system due to the problems we listed above.

The idea of a Mutual DAO focused on funeral plans is one aspect that I believe is the first of many applications of crypto & blockchain-based financial services for the mass market, but this kind of organisation can work best if a Mutual Assurance company were built today, let me tell why.

First, the properties of a Decentralized Autonomous Organisation (DAO) are similar to the properties of a Mutual Society:

- Mutual Society -> DAO

A DAO is a decentralized autonomous (governance) organization, an organisation that is meant to run autonomously without the normal structures of an organisation like a CEO with a board of directors.

- Pooled Capital -> Smart Contract

A smart contract is a self-executing contract with agreed-upon terms written in code.

- AGM -> Governance

- Benefits -> Profits

Second, the properties that govern DAOs and Mutual Societies are already engraved in the South African Mutual Life Assurance Society (Private) Act of 1966.

I. Incorporation of Society

(a) The South African Mutual Life Assurance Society act allows for the legal creation of an entity to “acquire & alienate property, enter into agreements and generally transact all its business.”

II. Business of Society

(a) The Society is empowered to carry out the business of a mutual life assurance & to grant the endowment to participate in the surplus & profits of the society or payment of money on any contigency event (death).

(b) to carry out accident assurance (death)

(c) “to grant, sell and purchase annuities of all kinds, whether dependent upon human life or otherwise, perpetual or terminable, immediate or deferred, contingent or otherwise;

(d) to realise any assets belonging to the Society when it may be necessary or advisable so to do;

(e) to re-assure any risk accepted by the Society and to undertake the re-assurance of risks accepted by any other person or body of persons: Provided that the risk so re-assured be one of those which the Society itself could have undertaken under the powers conferred by this Act;

(f) to lay out and invest the funds of the Society in any of the modes following–

(i) in the purchase of or advance on the public stocks, funds or debentures of the Government of the United Kingdom of Great Britain and Northern Ireland, of the Republic of South Africa or of any British Dominion, Colony or Dependency or any mandated territory of which Her Britannic Majesty or the Government of the Republic of South Africa holds mandate;” …

Maybe the last one needs a bit of updating but the overall act touches on key principles or properties with a high degree of similarity to existing organisations in the crypto sphere, just with a bit more clarity on important regulatory items like incorporation, the objects of the society, membership & governance. But based on the law it would be perfectly legal to set up a DAO-like insurance company

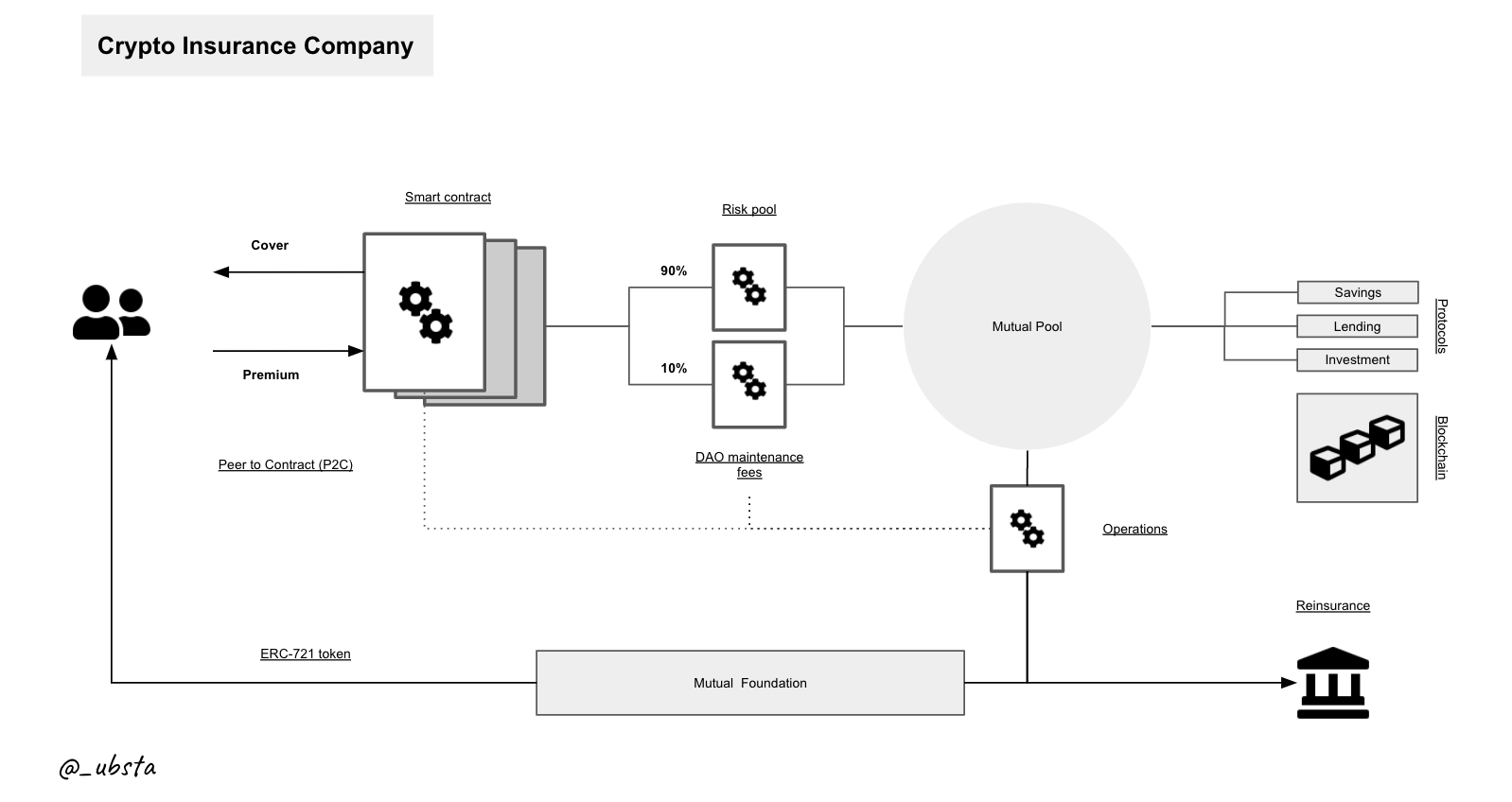

Executing a Crypto-Based Insurance Company

I touched on the why but I haven’t touched on the how. It would be a bit difficult if everything lived on the blockchain, the experience for the consumer would not be that great.

It’s very difficult to implement a fully decentralized insurance company on the blockchain. The best application is NexusMutual, which is a crypto-native insurance company that insures against a smart contract failure. That application is only native to the technology itself. For real-world application and mass adoption, implementation will need to hide the complexity from the end-user while reaching consensus.

Another crypto-native insurance project is Etherisc, a decentralized protocol on the Ethereum blockchain. Etherisc acts as a programmable protocol for various insurance products, like crop insurance, weather insurance and even social insurance.

Etherisc is a stab at what a decentralized insurance company should look like as a protocol. They have a high reliance on sovereign workers who are incentivized by percentage stakes on the premium the insured pays. But this model, even though it’s native to the blockchain, does not fully have the properties of a mutual society, the insured is not incentivized to participate in the upside of the protocol.

The execution of my model takes into account the properties of mutual societies. The insurance company exists for the benefit of its members by incorporating properties similar to DAOs in the crypto world.

Like normal insurance companies, the member pays a premium to cover funeral benefits but unlike traditional insurance companies the member contracts with the pool itself (smart contract), like peer-to-peer but instead its peer-to-contract. The smart contract, not the organisation governs terms. This autonomy creates trust in the decentralized insurance application. In the beginning, the execution and terms of the contract will be primitive but because it is funeral cover, the output is a zero-sum determination i.e “death, no death”.

Member funds are then pooled and invested in stablecoins via saving, lending, staking protocols with a significant chunk re-insured. Insurance is a scale game, but once there’s scale it’s pretty much everlasting. The most important part is the governance of the insurance application. An amendment of the South African Mutual Life Assurance Society Act caters for governance through polling:

9. (1) n the case of a poll being taken, every vote a members [will] be entitled to vote according to the following scale:…

(i) A member who is the holder of one or more policies but is not in receipt of any annuity shall be entitled to three votes, together with an, additional vote for each fifty rand, or portion thereof, forming part of the total premiums then payable per annum in respect of such policy or policies;

In the crypto world, people vote with their tokens, in this case, tokens would need to be distinctive to represent the individual and their policies. These tokens would be ERC-731 tokens, known as NFTs, an identifier of the policyholder(s) unique to other policyholders. The holder of the token would also be eligible for attributable benefits from the mutual pool profits, the NFT can act as a governance token. Coordinating this might seem like a nightmare, this is why the success will depend on the governance and coordination of the foundation until such time there can be sufficient decentralization.

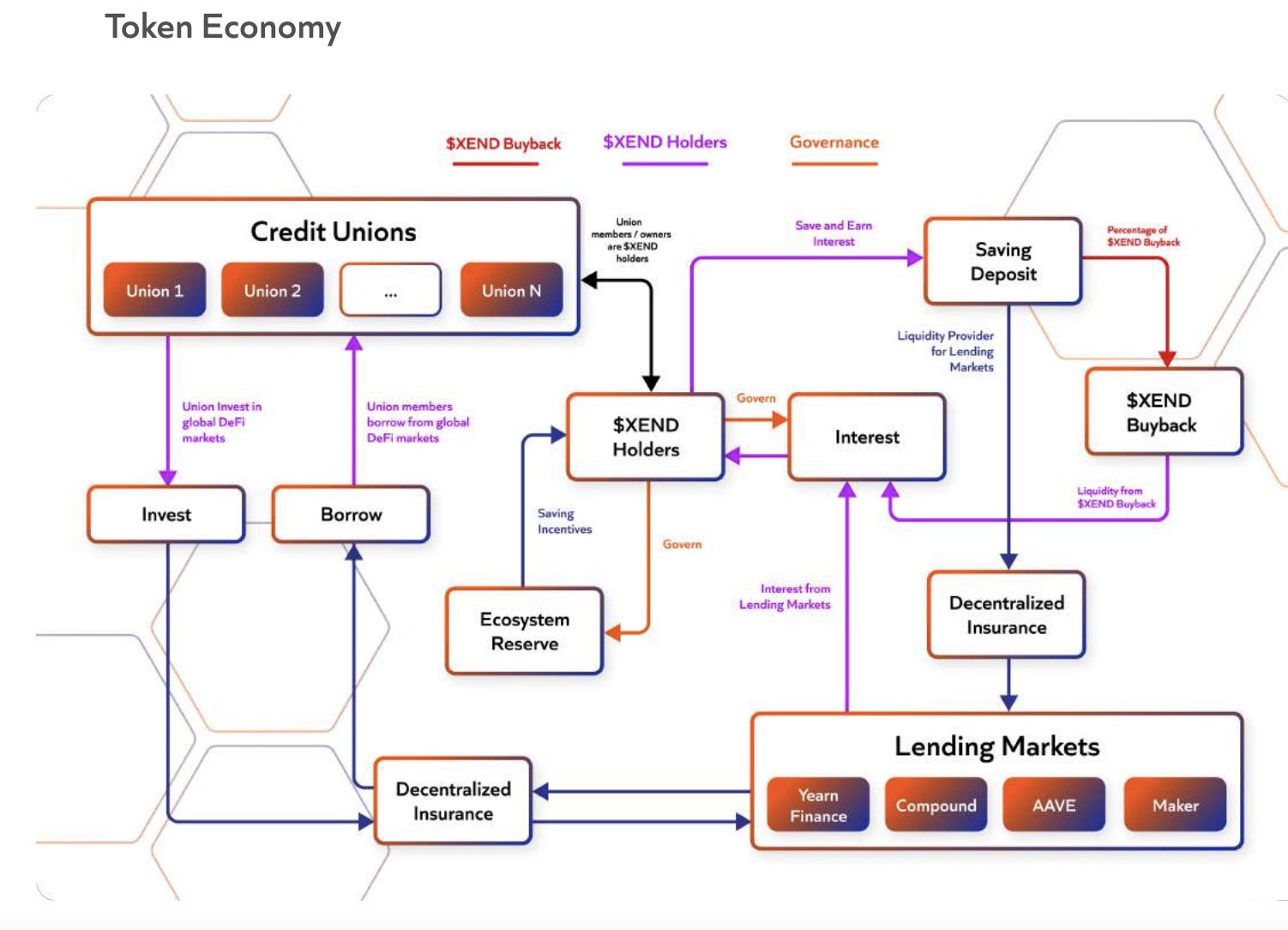

There have been some takes on crypto-based mutual societies, DAOs that do specific things, but these have been essentially groups of people organised on Discord servers to invest in crypto with some semblance of a governance structure. There’s a startup based in Nigeria called XendFinance that is having a go at creating a crypto-based credit union/cooperative, which is basically an aggregator of funds to invest in stablecoins. They are trying to create an ecosystem of decentralized credit unions/cooperatives.

The model looks a bit complex to me, a credit union, a cooperative & an insurance company are different types of organisations with different functions & different incentives regardless of incentives being monetary. But Xend is a good inference of the type of projects that are being created.

To conclude, the reason that it is probable that crypto-insurance companies will last a 100 years is the nature of insurance companies themselves, that the business is ultimately built around risk, the pricing, buying & selling of risk. The nature of risk will never change, risk is the product but how it’s bought & sold will change the nature of how business is done & how people organize themselves & capital. Just like how in the 17th-century people organized in mutual societies & how in the 19th century they organized in partnerships & how they organized in corporations in the late 20th century. It is quite plausible that the organization of people & capital will happen in DAOs as the 21st century progresses, which means insurance will be organized that way too. Thinking about the future is hard, understanding how the past happened makes it easier. This is one take at a 100-year company.

This is just a thought.

Take care.